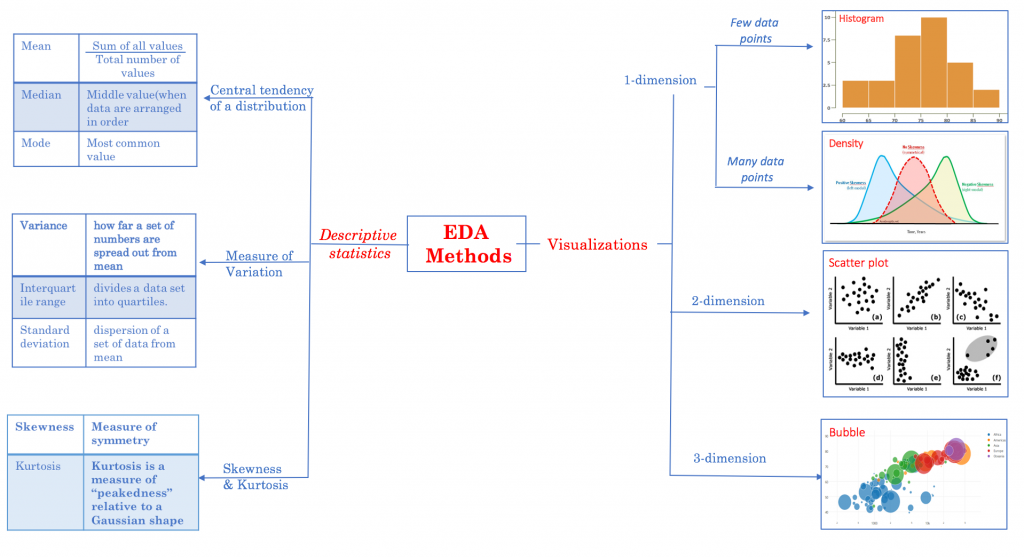

Python 演算法 Day 8 - 理论基础 统计 & 机率

Chap.I 理论基础

Part 4:统计 & 机率

Analyze the data through data visualization using Seaborn

5. Sampling Distributions 抽样分配

5-1. The Central Limit Theorem 中央极限定理

不论任何分配的母体,若样本够大,则每批样本的平均值 (X_bar) 的机率分配都会趋近常态分配(normal distribution)。

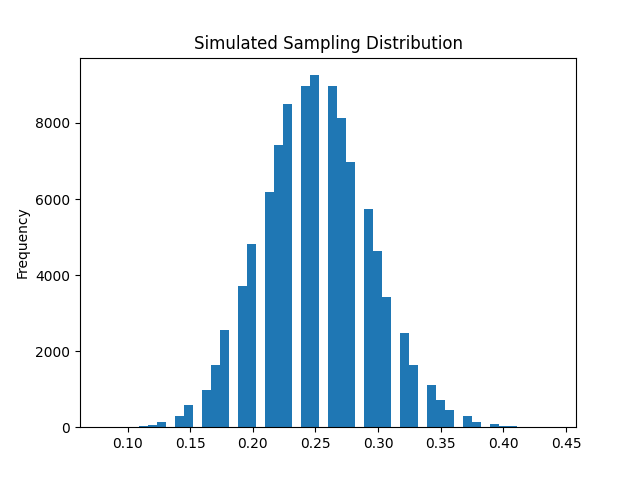

EX1. 抽取 10,000 批,每批 100 个样本,成功机率 0.25。

# 二项分配随机抽样 np.random.binomial(n, p, s)

# n: 每次抽样样本数

# p: 样本分配(母体机率)

# s: 抽样次数

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

n, p, s = 100, 0.25, 100000

X = np.random.binomial(n, p, s) # return 每次抽样成功次数 X

X_mean = X/n # 样本平均值

df = pd.DataFrame(X_mean, columns=['p-hat'])

print(df)

means = df['p-hat']

means.plot(kind='hist', title='Simulated Sampling Distribution', bins=50)

plt.savefig('pic 4-5 1')

plt.show()

print (f'Mean: {means.mean():.3f}')

>> Mean: 0.250

print (f'Std: {means.std():.3f}')

>> Std: 0.043

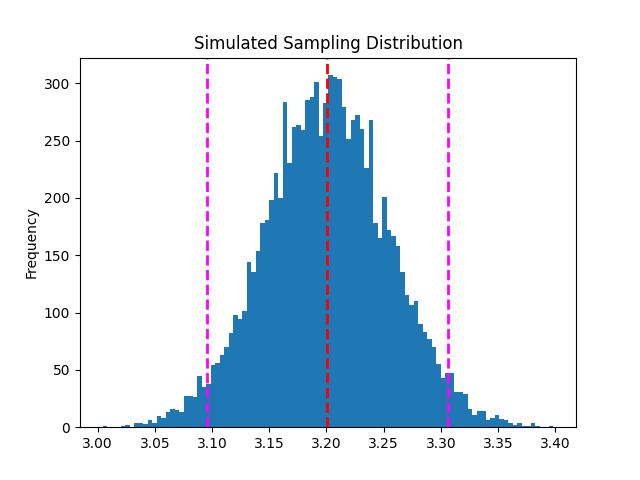

5-2. Confidence Intervals 信赖区间

基於某一信心水准(confidence level),例如95%,我们确信真实的参数值会落在特定区间内,称之。

信赖区间 = standard error x Z score

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

from scipy import stats

mu, sigma, n = 3.2, 1.2, 500

samples = list(range(0, 10000)) # 抽几次

X = np.array([])

X_bar = np.array([])

# np.random.normal(mean, std, n),return n-d array

for s in samples:

sample = np.random.normal(mu, sigma, n)

X = np.append(X, sample)

X_bar = np.append(X_bar, sample.mean())

df = pd.DataFrame(X_bar, columns=['X_bar'])

# 取得 X_mean 的 mean, std, 95% 信赖区间

m = df['X_bar'].mean() # X_bar 的平均

se = df['X_bar'].std() # 标准误

ci = stats.norm.interval(0.95, m, se) # return [m - 1.96 std, m + 1.96 std]

print (f'Sampling Mean: {m:.3f}')

>> Sampling Mean: 3.201

print (f'Sampling StdErr: {se:.3f}')

>> Sampling StdErr: 0.054

print (f'95% Confidence Interval: {ci}')

>> 95% Confidence Interval: (3.095256779885818, 3.3061798693546534)

# 作图

df['X_bar'].plot.hist(title='Simulated Sampling Distribution', bins=100)

plt.axvline(m, color='red', linestyle='dashed', linewidth=2)

plt.axvline(ci[0], color='magenta', linestyle='dashed', linewidth=2)

plt.axvline(ci[1], color='magenta', linestyle='dashed', linewidth=2)

plt.show()

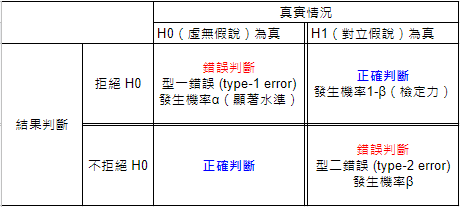

6. Hypothesis Testing 假设检定

首先有几个名词需要了解:

-

确认偏误(Confirmation Bias):人根据主观感受,而非客观资讯建立起主观以为的社会现实。

-

逻辑公理:

矛盾率:命题不可又真又假

排中率:命题只可以真或假

根据矛盾率,可以由假命题反证明真命题。 -

Null Hypothesis 虚无假设(H0):主张「母群参数与某数字之间无差别」

-

Alternative Hypothesis 对立假设(H1):主张「母群参数与某数字之间有差别」

-

虚无假设与对立假设两者必须互斥(有 A 没 B)且穷尽(包含所有)

6-1. Hypothesis Testing 假设检定

有了以上,接着我们进入假设检定

- 假设 H0 为真

- 以此为前提下,抽出这样的样本机率为?

- 若机率很小(10%? 5%? 1%? 0.1%?),则拒绝 H0(必须承受type I error)

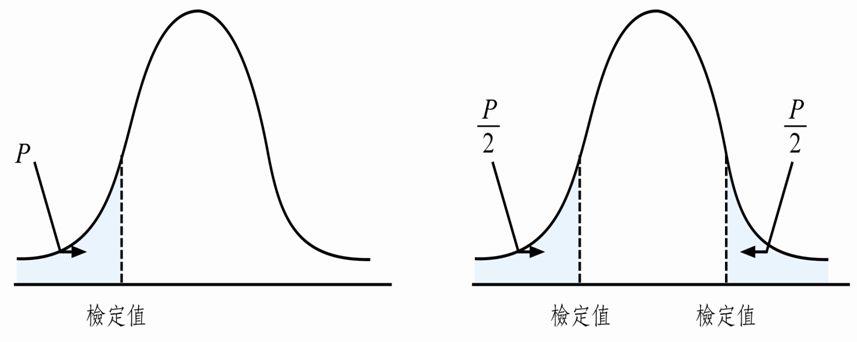

6-2. One-tailed test & Two-tailed test 单、双尾检定

顾名思义,单尾检定即假设拒绝区(critical value)仅有一边,其拒绝机率为 P。

反之,双尾检定即拒绝区包含两边,拒绝机率为 P/2。

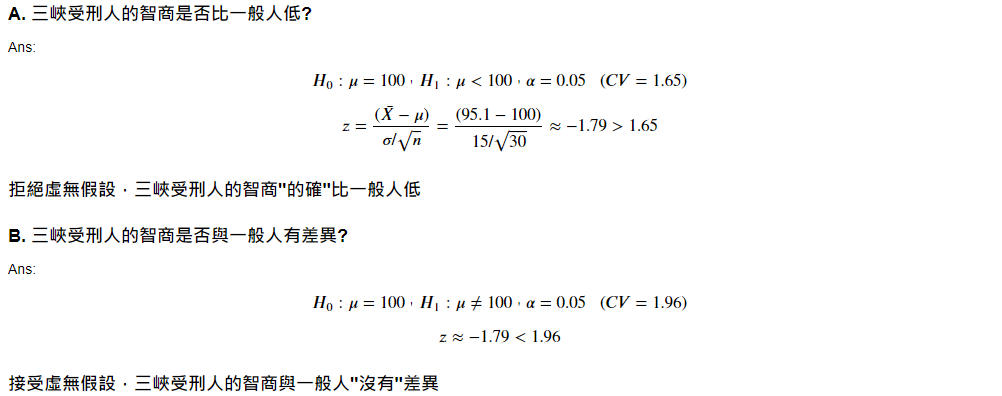

EX1. 一般人平均智商为100,标准差为15,呈常态分配。三峡典狱长挑选30位受刑人的随机样本,发现智商平均为95.1,请检测:

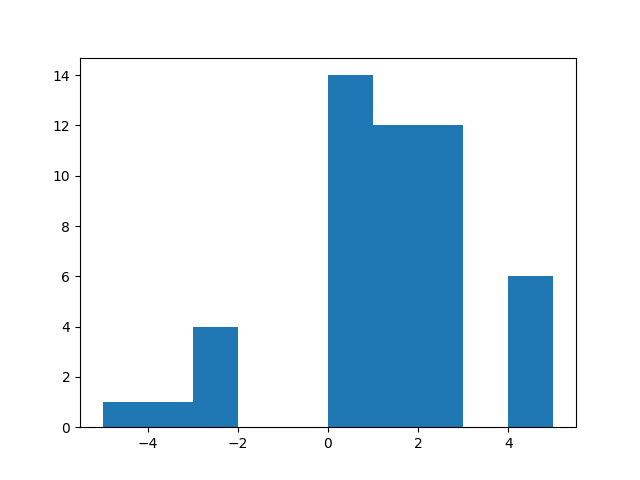

EX2. 学生为此课程打分,评分-5~5。请检测学生是否喜欢这门课程?

A. H0: u <= 0(学生不喜欢)

B. H1: u > 0 (学生喜欢)

C. alpha = 1.645 (90%)

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(123)

low = np.random.randint(-5, -1, 6)

mid = np.random.randint(0, 3, 38)

high = np.random.randint(4, 6, 6)

sample = np.append(low, np.append(mid, high))

print("Min:" + str(sample.min()))

print("Max:" + str(sample.max()))

print("Mean:" + str(sample.mean()))

plt.hist(sample)

plt.show()

6-3. Z-test/t-test t/z 检定

- z-test:资料必须是随机样本,且母体来自常态分配,母体标准差已知。

- t-test:资料必须是随机样本,且母体来自常态分配,母体标准差未知,以样本标准差取代。

- 单样本(single sample):检定一组样本平均与母体平均是否有差异

- 双样本(two sample):检定两组样本平均之间是否有差异

A. 单样本单尾检定:sample 有无显着大於 0?

from scipy import stats

import numpy as np

import matplotlib.pyplot as plt

# 样本(平均 0、标准差 1.15、抽取 10000 次)

sample = np.random.normal(0.5, 1.15, 100)

# scipy.stats.ttest_1samp(a, mother, alternative='two-sided') # 单样本检定

# a: 样本

# mother: 母体

# alternative: 'two-sided'(双尾), 'less', 'greater'(左/右尾)

z, p = stats.ttest_1samp(sample, 0, alternative='greater')

print(f'z-statistic:{z}')

>> z-statistic:3.9074479639245183

print(f'p-value:{p}')

>> p-value:8.53595856851376e-05

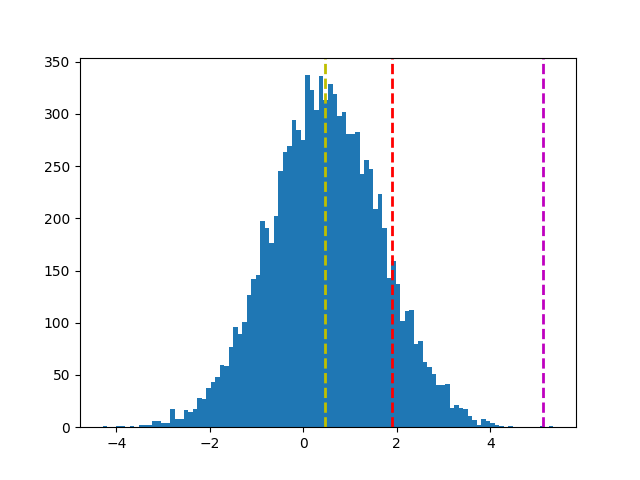

x_bar = np.random.normal(sample.mean(), sample.std(), 10000)

plt.hist(x_bar, bins=100)

plt.axvline(x_bar.mean(), c='y', linestyle='--', linewidth=2)

# 计算信心水准 95%,右尾检定结果(右边 5%)的 x_bar 值

ci = stats.norm.interval(0.90, 0, 1.15) # 此函数仅能计算双尾

plt.axvline(ci[1], c='r', linestyle='--', linewidth=2)

# 根据 mean + t*s 划出对立假设 x_bar 落点

plt.axvline(x_bar.mean() + z*x_bar.std(), c='m', linestyle='--', linewidth=2)

plt.show()

结论:紫色落於红色外,拒绝虚无假设。sample 有显着大於 0。

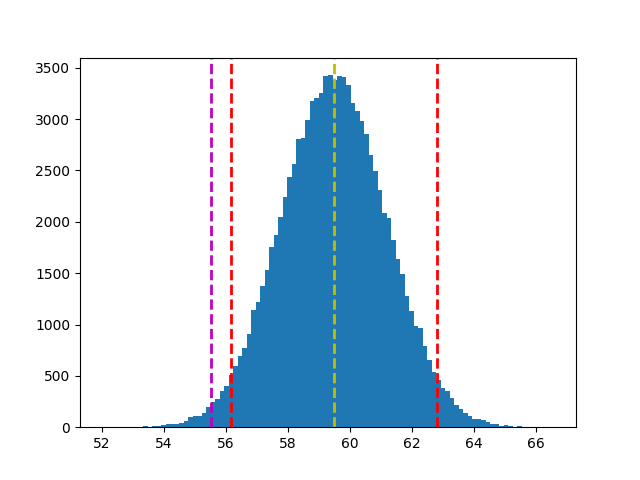

B. 双样本单尾检定:sample1 有无显着异於 sample2?

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

np.random.seed(123)

sample1 = np.random.normal(59.45, 1.5, 100)

sample2 = np.random.normal(60.05, 1.5, 100)

# scipy.stats.ttest_rel(a, b, alternative='two-sided') # 双样本检定

# a & b: 样本

# alternative: 'two-sided'(双尾), 'less', 'greater'(左/右尾)

t, p = stats.ttest_rel(sample1, sample2) # , alternative='greater'

print(f't-statistic:{t}')

>> t-statistic:-2.3406857739212583

print(f'p-value:{p}')

>> p-value:0.021254108930688475

# 根据 sample1 平均值 & 样本标准差,划出抽取 100000 次(每次100批)分配

s1_bar = np.random.normal(sample1.mean(), sample1.std(), 100000)

plt.hist(s1_bar, bins=100)

plt.axvline(s1_bar.mean(), c='y', linestyle='--', linewidth=2)

# 计算信心水准 95%,右尾检定结果(一边 5%)的 x_bar 值

ci = stats.norm.interval(0.95, s1_bar.mean(), s1_bar.std())

plt.axvline(ci[0], c='r', linestyle='--', linewidth=2)

plt.axvline(ci[1], c='r', linestyle='--', linewidth=2)

# 根据 mean + t*s 划出对立假设 x_bar 落点

plt.axvline(s1_bar.mean() + t*s1_bar.std(), c='m', linestyle='--', linewidth=2)

plt.show()

结论:sample1 显着不同於 sample2

.

.

.

.

.

Homework Ans:

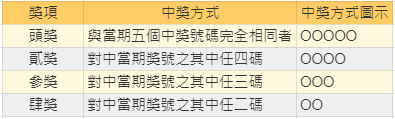

#1. 今彩 539 (https://www.taiwanlottery.com.tw/dailycash/index.asp)

- 请问各个奖项中奖机率为?

- 请问每张彩券平均报酬率?

各奖项的中奖方式如下表:

奖金如下:

解答如下:

import scipy.special as sps

import numpy as np

name = ['头奖', '二奖', '三奖', '四奖']

bonus = [8000000, 20000, 300, 50]

total = []

for i in range(4):

prob = sps.comb(5, 5-i) * sps.comb(34, i) / sps.comb(39, 5)

money = sps.comb(5, 5-i) * sps.comb(34, i) * bonus[i]

total.append(money)

print(f'{name[i]} 中奖机率为: {prob*100 :.4f} %')

gain = np.array(total).sum()/sps.comb(39, 5)

cost = 50

print()

print(f'平均每注中奖金额: {gain :.2f}')

print(f'平均每注投报率为: {(gain-cost)*100/cost :.2f} %')

>> 头奖 中奖机率为: 0.0002 %

二奖 中奖机率为: 0.0295 %

三奖 中奖机率为: 0.9744 %

四奖 中奖机率为: 10.3933 %

平均每注中奖金额: 27.92

平均每注投报率为: -44.16 %

#2. 使用 sklearn 内建资料集 "load_boston" 来预测波士顿房价

A. 一次回归求解:

# A-1. Data prepare 准备资料

from sklearn import datasets

ds = datasets.load_boston()

import pandas as pd

X = pd.DataFrame(ds.data, columns=ds.feature_names)

y = ds.target # 房价

# A-2. Data clean 资料清理

print(X.isnull().sum().sum())

>> 0

# A-4. Split 拆分资料

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size = 0.2)

# A-3. Feature Engineering 特徵工程

# 标准化、归一化,严谨的作法是放在 4. Split 後,以此避免训练资料与测试资料互相干扰。

from sklearn.preprocessing import StandardScaler

scaler = StandardScaler()

X_train = scaler.fit_transform(X_train) # 训练资料要特徵缩放

X_test = scaler.transform(X_test) # 测试资料则仅做特徵转换

# A-5. Train Model 机器训练

from sklearn.linear_model import LinearRegression

clf = LinearRegression()

clf.fit(X_train, y_train)

print(clf.coef_) # 回归线系数

>> [-0.73333119 1.29309093 0.15261025 0.61015457 -2.18126673 2.48140152

0.18613576 -3.10258233 2.78838943 -2.32101423 -1.97367244 0.76910136

-4.00329437]

print(clf.intercept_) # 回归线偏差值(截距)

>> 22.450247524752527

# 最大影响因子

import numpy as np

print(ds.feature_names[np.argmax(clf.coef_)]) # 系数最大项

>> RAD

print(np.max(clf.coef_)[::-1]) # 值

>> 2.78838943

# A-6. Score Model

score = clf.score(X_test, y_test)

print('Model Score:', score)

>> Model Score: 0.7445778921293265

# 计算 MSE (mean square error)

from sklearn.metrics import mean_squared_error

MSE = mean_squared_error(y_test, clf.predict(X_test))

print('MSE=', MSE)

>> MSE= 21.285739578017278

# 均方根误差

RMSD = mean_squared_error(y_test, clf.predict(X_test)) ** .5

print('RMSD=', RMSD)

>> RMSD= 4.61364710159081

# 判定系数(之後会讲)

from sklearn.metrics import r2_score

judge = r2_score(y_test, clf.predict(X_test))

print('R2 Score=', judge)

>> R2 Score= 0.7445778921293265

B. 二次回归

一次回归结果看来准确率还不够高,

我们可以用 sklearn 中的 PolynomialFeatures 调整自由度为 2:

# B-1. Data prepare 准备资料

from sklearn import datasets

ds = datasets.load_boston()

import pandas as pd

X = pd.DataFrame(ds.data, columns=ds.feature_names)

y = ds.target # 房价

# 使用 sklearn 中的 PolynomialFeatures 转换为二次回归

# 预设 degree=2,即 Y 会由 [1, a, b, a^2, ab, b^2] 组成

from sklearn.preprocessing import PolynomialFeatures

poly = PolynomialFeatures(degree=2)

X2 = poly.fit_transform(X)

# B-2. Data clean 资料清理

# B-4. Split 拆分资料

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X2, y, test_size = 0.2)

# B-3. Feature Engineering 特徵工程

from sklearn.preprocessing import StandardScaler

scaler = StandardScaler()

X_train = scaler.fit_transform(X_train) # 训练资料特徵缩放

X_test = scaler.transform(X_test) # 测试资料仅做转换

# B-5. Train Model 机器训练

from sklearn.linear_model import LinearRegression

clf = LinearRegression()

clf.fit(X_train, y_train)

# B-6. Score Model

score = clf.score(X_test, y_test)

print('Model Score:', score)

>> Model Score: 0.8832125484403865

# 计算 MSE (mean square error)

from sklearn.metrics import mean_squared_error

MSE = mean_squared_error(y_test, clf.predict(X_test))

print('MSE=', MSE)

>> MSE= 10.88594930129324

# 均方根误差

RMSD = mean_squared_error(y_test, clf.predict(X_test)) ** .5

print('RMSD=', RMSD)

>> RMSD= 3.299386200688431

C. 矩阵公式

最後,我们用矩阵公式 A = (X'*X)^-1*X'*Y求解:

# C-1. Data prepare 准备资料

from sklearn import datasets

ds= datasets.load_boston()

import pandas as pd

X = pd.DataFrame(ds.data, columns=ds.feature_names)

y = ds.target

# print(X.head())

# C-4. Split 拆分资料

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size = 0.2)

# C-5. 矩阵运算

# 最後一行补1

import numpy as np

b_train = np.ones((X_train.shape[0], 1))

# print(b_train.shape) # (404, 1)

# 黏合

X_train=np.hstack((X_train, b_train))

# # 套用公式 A = (X' * X)^-1 * X' * Y

# print(X_train.T.shape) # (14, 404)

# print(X_train.shape) # (404, 14)

# print(y_train.T.shape) # (404,)

A = np.linalg.inv(X_train.T @ X_train) @ X_train.T @ y_train

print(A.shape)

# matrix(X_train, y_train)

# # 计算 MSE (mean square error)

# print(X_test.shape) # (102, 13)

# print(y_test.shape) # (102,)

b_test = np.ones((X_test.shape[0], 1))

# print(b_test.shape) # (102, 1)

# 黏合

X_test=np.hstack((X_test, b_test))

MSE = np.sum((X_test @ A - y_test) ** 2) / y_test.shape[0]

print('MSE=', MSE)

>> MSE= 17.679787655718744

# 均方根误差

RMSD = MSE ** 0.5

print('RMSD=', RMSD)

>> RMSD= 4.204733957781246

.

.

.

.

.

Homework:

使用假设检定,检定近40年(10届)美国总统的身高是否有差异?

(Data: president_height.csv)

<<: Day 7 - Rancher 系统管理指南 - RKE Template

>>: Day 07 Azure cognitive service- 於是,Chatbot 也有了智慧

Android学习笔记30

昨天做完了验证码,那今天就把他加入到帐号密码之中 首先要先建立一个imageview来存放验证码,并...

【DAY 8】SharePoint 的应用五花八门,什麽最适合你?(上)

哈罗 ~ 大家好,希望昨天的文章有让大家更认识 SharePonit 这个工具到底可以用来做什麽。昨...

Android学习笔记24

今天来用checkbox首先先在xml新增 <CheckBox android:id=&quo...

Backtrader - 策略收益

以下内容皆参考 Backtrader 官网 昨天介绍了 backtrader 如何去执行一个策略,今...

day 21 - NSQ Producer

Producer是讯息发送方, 他会对nsqd发送讯息, nsqd支援TCP(port:4150) ...